The Golden Thread of Capital Market Innovation

The Known-Knowns for Capital Market Entrepreneurs

The Golden Thread of Ariadne helped Theseus find his way out after slaying the Minotaur in the infamous Labrynth.

In a vain attempt at the same for capital markets entrepreneurs, let me attempt to explain the golden thread of capital market innovation. Unlike other sectors, the Capital Market entrepreneurial landscape (save for BioTech and Pharmaceuticals) provides unique and unexpected challenges to the innovator.

Here are a few things to consider:

You’re in this for a multi-decade ride

Every Asset-Class is astronomically different

There are more people to consider than the customer

Incumbents will fight against and win against emerging technologies

Capital Market Change is a Multi-Decade Ambition!

I will provide two close-to-heart examples of the extent of time needed for “basic” market consensus around critical infrastructure. For some of you – this may give you flashbacks… I am talking about 1) the Consolidated Tape in the UK and European Markets and 2) in the US, FINRA’s TRACE. Both of these sagas seem to end, begin, and end again for at least the last 40 years.

Ironically, you always hear Americans talking about the “slow Europeans,” but the nuance in this is that Europe needs to balance 27 national juristidications unlike the US; who has a single federal regulation policy that supersedes state laws.

Even so, the United States took decades to introduce its rather lackluster, yet still impactful TRACE (Transaction Reporting and Compliance Engine) system. Let’s trace (no pun intended) a quick history of how long it took to create a sliver of transparency in the US.

Pre-1980s, little transparency.

1980s, M&A Junk Bond Craze (Initiated and Powered by Drexel Burnham Lambert and Michael Milken - you might’ve heard of the Milken Institute).

1989, Junk Bond Market Crash.

1991, Introduction of FIPs (Fixed Income Pricing System) starting with 50 High-Yield Bonds.

1998, “FIPs does not do enough.”

2002, The introduction of TRACE with a 75-min reporting window for transactions with a “phased-in” approach.

2005, the TRACE reporting window shortened to 15-minutes where it is today (2025) with no insights into actual trade size, besides pre-determined “trade size” plugs that vary month to month.

2006, TRACE began real-time TRACE dissemination upon reporting-party receipt.

In 2005, SEC Commissioner, Roel Campos said in Japan:

“The U.S. moves on corporate bond transparency emanated from two requests from the SEC to the National Association of Securities Dealers (NASD). In 1991, former SEC Chairman Breeden asked the NASD to create a system to promote transparency in liquid high-yield corporate bonds following insider trading and price manipulation scandals in the bond markets in the late 1980’s. The Commission sought to avoid another scandal such as the one that lead to the demise of Drexel Burnham Lambert. As a result, the NASD created the Fixed Income Pricing System (FIPS), which provided transparency for 50 liquid high-yield bonds.

In 1998, former Chairman Levitt noted that the FIPS initiative did not go far enough, remarking that “[t]he sad truth is that investors in the corporate bond market do not enjoy the same access to information as a car buyer or a homebuyer or, dare I say, a fruit buyer.” To address the lack of price transparency in the corporate debt market, Chairman Levitt called on the NASD to do three things: (1) Adopt rules requiring dealers to report all transactions in U.S. corporate bonds and preferred stocks to the NASD and to develop systems to receive and redistribute transaction prices on an immediate basis; (2) Create a database of transactions in corporate bonds and preferred stocks. This would enable regulators to take a proactive role in supervising the corporate debt market, rather than only reacting to complaints brought by investors; and (3) In conjunction with the development of a database, create a surveillance program to better detect fraud in order to foster investor confidence in the fairness of these markets. As a result, broker-dealers must now report all Over-the-Counter (OTC) corporate bond transactions to the NASD’s Transaction Reporting and Compliance Engine (TRACE) System.”

The moral of the story is that even spurred by crises, market abuses, and public outrage, it still took the United States over two decades to pass a semblance of transparency (and I might add only in post-trade transaction reporting).

And that semblance remains the ground-truth for many firms 20 years later, in a market with idiosyncratic instruments and variable trade frequency, there are still many questions left to discuss about bond market transparency, including:

Does a trade that happened weeks ago still represent the best price today?

Does my relationship to the dealer matter more than the actual pricing of the instrument?

Are new issues being priced fairly to all?

And this conversation until now says nothing of pre-trade data at the institutional level (let alone retail)!

The truth holds globally for capital markets: Innovation is a multi-decade project with many interested parties decreeing opinions about the correct path forward.

Capital Market Innovation is Asset-Class Dependent!

This part should be perfectly understandable now!

Market Innovation in every asset-class is on a different trajectory balancing different perspectives – and that’s the heart of the markets, in theory, according to market participants, every asset-class presents its own unique challenges and considerations.

Many hold differing opinions on this, but I believe the ground truths hold across asset-classes; transparent pre-trade, timely post-trade reporting, and efficiency in settlement processes are instrumental in accelerating the growth and mobility of any asset-class and global markets (could we agree on that?).

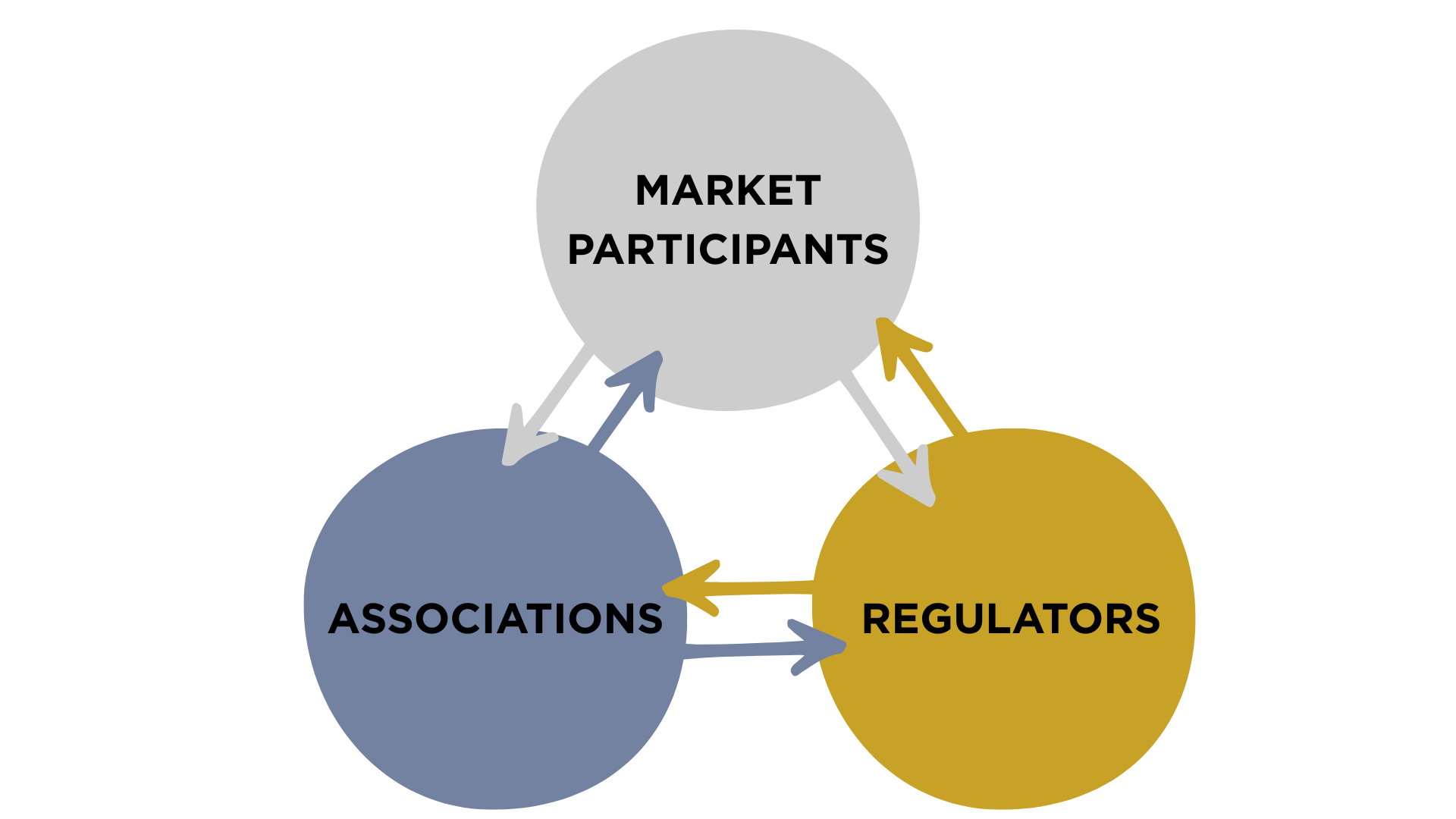

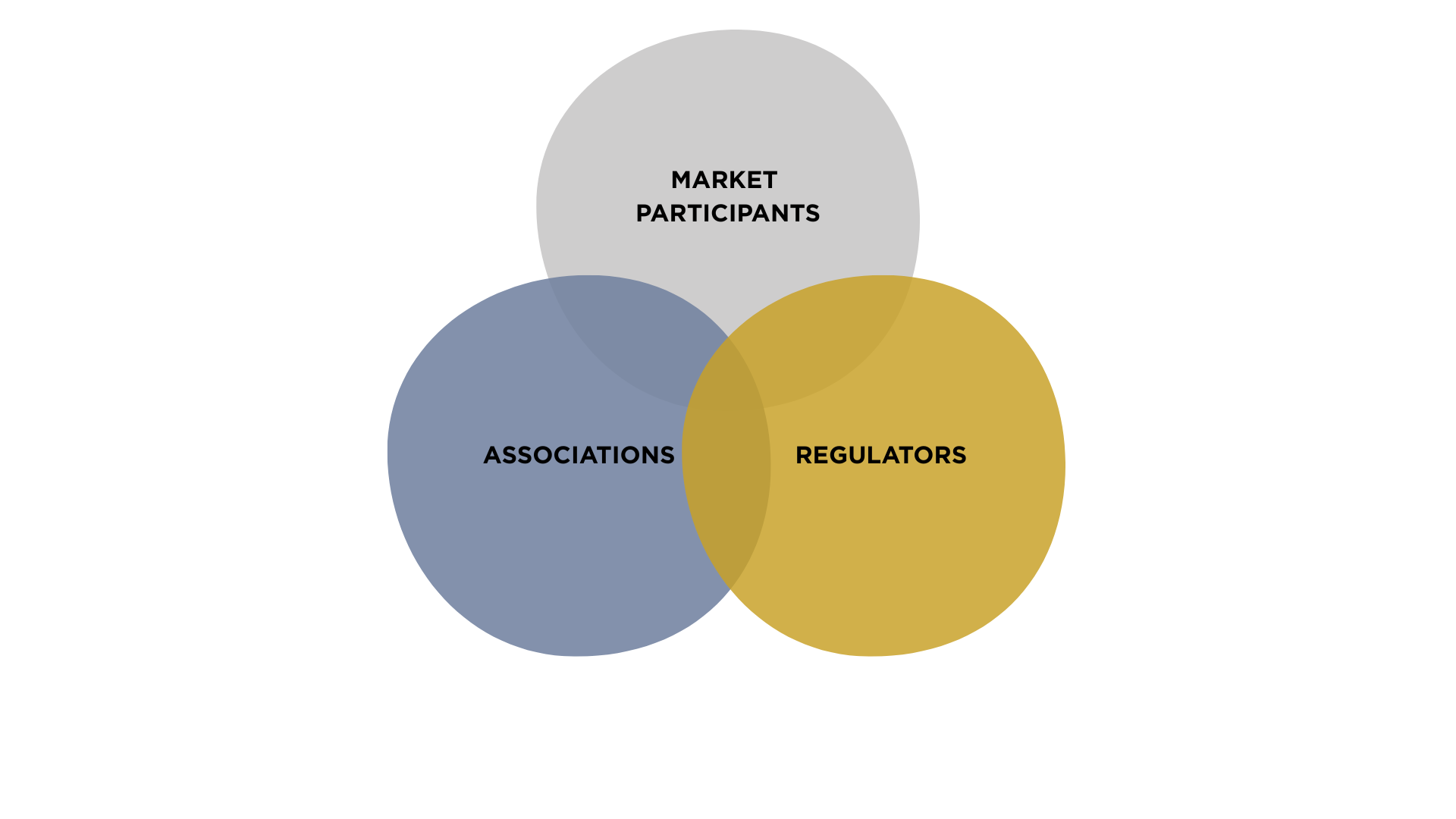

There are more voices than just the customers!

For the uninitiated, the truth lies in balancing the voices that make innovation possible. Begin with naming them — here are the three entities to consider when seeking to innovate in the Capital Markets:

Market Participants

Associations

Regulators

Each of these groups are working to create a market in their own vision. Market Participants, typically, are seeking to increase business and bottom-line. Associations are seeking to balance the conversations between Market Participants and Regulators. And Regulators are seeking to make a more equitable and less manipulation-prone market. In some ways, these groups hold similar values on some topics creating overlap in agendas at times:

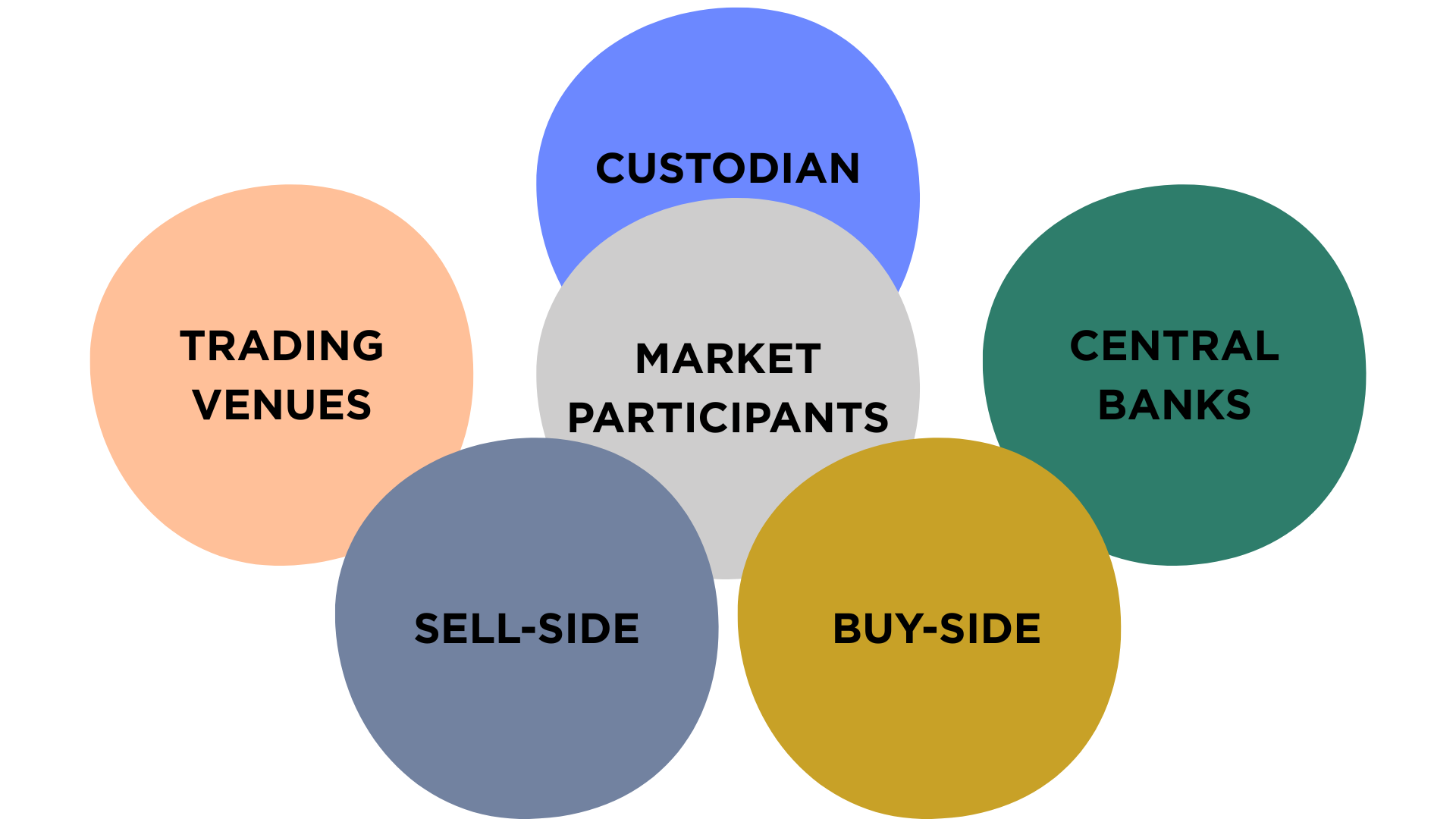

When all the groups align we call it total market consensus. The first and hardest challenge that kills most start-ups is aligning the market consensus of Market Participants, because of the diversity of opinions among market participants. Market Participants are not monolithic; they all hold different stances, and let’s list a few types of Market Participants to consider:

Central Banks

Custodians

Sell-Side

Buy-Side

Trading Venues

All of these Market Participants have their own dynamic view on the markets, and that dynamic view will continue to evolve as technology, trading, relationships, and regulations change throughout time, but there are some grounding truths for each participant that we can get into, but let’s save that for another article.

Understanding these Market Participants’ points of view is critical to understanding if the innovation you are proposing will gain traction or become another speck of sand in the deserts of attempted past innovations.

Once you understand the real views of these Market Participants, then you are in a better position to pinpoint your customer’s actionable pain points and provide a coherent solution. Often times, I see both young and experienced ambitious entrepreneurs attempting to solve a problem that there is indeed no market for solving! Leading me into my last point – the incumbents (or winners of today) will fight you every step of the way and win if you are trying to eat into their margins.

Incumbents will fight and win!

New founders underestimate the power of the incumbent in the Capital Markets – unlike traditional retail-focused Financial Technology institutional FinTech is dependent on institutional support.

Retail-focused FinTech can run around to run-of-the-mill Venture Capitalists to find funding that can turn dreams into reality seemingly overnight. These innovators will face few obstacles standing in their way outside of the traditional problems with sales and marketing, and little concern about 100-year strategies.

Institutional-focused FinTech is slow, treacherous, political, and long-term oriented – the goal of the start-up in Institutional FinTech is to be around for ten or twenty years, then institutions will start to take you seriously (there are edge-cases of fast success, but oftentimes it’s accompanied with a crash and burn).

Institutional-focused FinTech takes white papers, association-level negotiation, and regulatory alignment. And the truth is, if your innovation is going to eat into an incumbent’s profits, the incumbents will fight you tooth and nail to keep you on the sidelines – conversations will be had behind closed doors, wheels will be greased against you, and suddenly there will be a new regulatory discussion with you in the cross-hairs.

Sometimes, in a seemingly about-face, your solution will now be discussed as a public utility instead of a private enterprise, threatening your whole business model. I have seen it before, and it will happen again.

This article is not meant to dissuade you from innovating in the markets; I am trying to provide you with the golden thread for creating sustainable and successful innovation in Capital Markets by letting you know the real obstacles in front of you!

So what do you need to do to find success:

Know this is a long-term endeavour and do not lose sight of your mission!

Intimately know and be an expert in your asset-class!

Understand the voices and create enduring alliances early on!

Disarm the incumbents, make the incumbents money in the process, and create allies out of the incumbents quickly!

I hope this helps!

Let’s get to work!